This post will discuss how SVIX works, including how it trades, how its value is established, what it tracks, tax treatment, termination risk, likely liquidity, and performance simulations.

Volatility Shares’ -1x Short VIX Futures ETF (ticker: SVIX) started trading Wednesday, March 30th, 2022 After a gap of four years, volatility traders regained access to a -1X leveraged short-term volatility Exchange Traded Fund (ETF). SVIX’s Prospectus is available on the Volatility Shares site.

Before we get into the specifics of how SVIX works, I’m disclosing that I hold a small, minority share in Volatility Shares LLC, the issuer of SVIX. Volatility Shares has also issued BITX, ZIVB, ETHU, and UVIX ETFs. I do not hold management, executive, or operational roles in Volatility Shares LLC, nor do I give recommendations or investment advice to their clients. My analysis of these funds and their associated indexes is my own, is not investment advice, and is based on publicly-available information.

What’s Different About SVIX?

A major difference between SVIX and the previous -1X leveraged short term volatility funds VelocityShares’ XIV and ProShares’ -1X SVXY (which reduced its leverage to -0.5X in February 2018) is that SVIX uses the Cboe’s new Short VIX Futures Index (ticker: SHORTVOL). SHORTVOL differs from the SPVXSP/SPVXSTR indexes used by the other short-term volatility Exchange Traded Products in that it uses a time-weighted average of the underlying VIX futures’ last price and their Trade-At-Settlement (TAS) order spread, taken every 5 seconds in the last 15 minutes before closing, to calculate its end-of-day closing value.

The use of the SHORTVOL index makes SVIX less sensitive to the sometimes-treacherous end-of-day dynamics of the market. For details on the SHORTVOL index and how it would have performed compared to the other short term volatility indexes since December 2005, see “Why We Need the New SHORTVOL & LONGVOL indexes.” SVIX is complemented by the new UVIX, a +2X leveraged ETF, which seeks to achieve double the percentage moves of the LONGVOL index on a daily basis. For more information on it see “How Does UVIX Work?

The other significant difference between SVIX/UVIX and previous short term volatility funds is that operationally they limit their total participation in the VIX Futures market. When rebalancing they will limit their trades to be no more than 10% of the market volume in any 15-minute period of continuous market trading, including after-hours trading. To my knowledge, this is an unprecedented operational constraint for an Exchange Traded Product. Rebalancing is an operational process (described later in this post), used by leveraged funds to achieve their target leverage. The net effect of this rebalancing restriction is to structurally prioritize the smooth functioning of the market over the precise tracking of SVIX/UVIX share prices to their underlying indexes. I believe this constraint will not only benefit the VIX futures market, but UVIX/SVIX shareholders as well.

How does SVIX trade?

- SVIX trades like a stock. It can be bought, sold, or sold short any time the market is open, as well as pre-market and after-market periods.

- SVIX has options available now. Unlike most options, options on volatility ETPs, including SVIX, continue trading for 15 minutes after the NYSE close. Strikes are currently available at dollar increments from $5 to $25. Bid/ask spreads will likely be wide while volumes build. Unless it is a very liquid option market, like SPY, I use limit orders with option trades with starting prices around the midpoint between bid and ask prices. I usually get fills at the midpoint, or after I’ve sweetened the deal a few dollars in the market makers’ direction.

- SVIX’s shares can be split or reverse split—but unlike long volatility funds such as VXX (with 8 splits since inception), splits of SVIX will be an infrequent event

- SVIX is tradable in most IRAs/Roth IRAs, although your broker will require you to electronically sign a waiver that documents various risks. Shorting of any security is not allowed in an IRA.

How is SVIX’s price established?

- The bid and ask prices of SVIX should typically be close to its Indicative Value (IV) price. The IV price is the per-share value of the fund’s underlying assets minus fees and operational costs. During periods of heavy selling/demand, the bid/ask prices might start moving away from the IV price. If SVIX’s prices start diverging from its IV value during regular market hours then market makers and wholesalers called “Authorized Participants” (APs) will likely intervene by buying or selling shares of SVIX. If SVIX is trading enough below its IV price they will start buying large blocks of SVIX—which tends to drive the price up. If it’s trading high, they will short SVIX. The APs have an agreement with VolatiltyShares that allows them to do these restorative maneuvers at a profit, so they are highly motivated to keep SVIX’s tracking in good shape. For more information on these behind-the-scenes arbitrage processes see Why Arbitrage is Essential For Exchange Traded Products.

- SVIX will likely register gains during rising market periods but will experience dramatic drawdowns when markets are in turmoil. The chart below shows a simulation of SVIX from December 20, 2005, using the SHORTVOL index values. The simulation assumes SVIX has an annual fee of 1.35% and an estimated 0.63% per year in additional fixed and operational costs.

- SVIX’s potential for big drawdowns is shown in this simulation with a 39% drawdown in February 2018 and 87% in March 2020 during the Covid crash.

- SVIX seeks investment results before fees and other expenses that correspond to the daily moves of the SHORTVOL index. This index is maintained by the Cboe and its values are published during market hours. SHORTVOL values can be found on the CBOE Index Dashboard and Yahoo Finance as ^SHORTVOL. The Net Asset Value/Indicative Value (NAV/IV) values for SVIX are published by Trading View and the Cboe. I offer a free spreadsheet with simulated close values for SVIX and UVIX since December 2005.

What is SVIX’s Market Strategy?

- The term structure of VIX futures is contango about 80% of the time, with prices increasing with additional time to expiration. Unless there is a significant turmoil in the market the futures usually decay significantly in value over time when they are in this configuration. Since SVIX is short VIX futures, it’s positioned to benefit from that decay.

- This situation sounds like a short seller’s dream, but VIX futures occasionally go on an upward tear, punishing those that are short volatility.

- SVIX does not behave like a static short position. It attempts to track the SHORTVOL index, which moves the opposite direction of a long volatility position. To accomplish this strategy SVIX must rebalance its investments near the end of each day. For a detailed example of what this rebalancing looks like see “How do Leveraged and Inverse ETFs Work?”

- There are some very good reasons for this rebalancing strategy, for example, a static short can only produce at most a 100% gain and the leverage of a static short is rarely -1X (for more on this see “Ten Questions About Short Selling”). SVIX, on the other hand, should be able to deliver a move very close SHORTVOL’s percentage daily move on an ongoing basis.

- Detractors of the daily rebalancing approach correctly note that SVIX and funds like it often suffer from volatility drag. If a long volatility fund like VXX moves around and then ends up in the same place SVIX will lose value, whereas a static short of VXX would not. However, as I discussed in “Is Shorting UVIX, UVXY or VXX the Perfect Trade?”, static short positions have other problems.

- While volatility drag often reduces performance, daily resetting funds like SVIX don’t always underperform. If VIX futures are trending down, they can deliver better than -1X cumulative performance. For more on this phenomenon see “Sometimes Leveraged Funds Outperform.”

Can SVIX Terminate?

SVIX doesn’t have a percentage decline trigger as XIV did, but it can terminate, as can any Exchange-Traded Product. In the Prospectus (on approximately page 86) it says:

Termination Events

The Trust, as the case may be, the Funds, may be dissolved at any time and for any reason by the Sponsor with written notice to the shareholders.

- The prospectus does guarantee that SVIX will not go below zero in value, so it is almost certain the fund would terminate if its mix of VIX futures reached or exceeded a +100% move in value in a day.

- Because SVIX rebalances assets each day the multi-day performance is unimportant from a termination standpoint. For example, if SVIX went down 40% three days in a row it would experience a severe drawdown, minus 78.4% to be exact, but not the 120% sum of the losses. Unless intra-day losses approach 100% SVIX would not be forced to terminate.

What is SVIX’s Tax Treatment?

- Because SVIX takes positions in VIX futures, the IRS views its shareholders as partners that need to file K-1 forms for taxable accounts at tax time. This adds some complexity to tax reporting but it also has some potential benefits, for example, gains may qualify for treatment as 1256 contracts, where gain/loss are split 60% long-term and 40% short term regardless of how long you held the shares.

- Be aware that brokers sometimes incorrectly report information on K-1 type ETPs via the 1099 form method.

- Proshares’ UVXY & SVXY volatility ETFs require a similar K-1 tax style treatment. Their Tax Information FAQ page gives additional information on K-1 tax reporting.

- I am not a tax advisor, but my understanding is that SVIX held in non-taxable accounts such as IRAs will not require tax reporting.

How Good is SVIX’s Liquidity?

- With bid/ask spreads of a cent or two and average daily volumes around one million SVIX is showing very good liquidity. As I discuss in Evaluating the Liquidity of Low Volume Exchange Traded Funds, the key liquidity source for ETPs is the liquidity of the underlying security, which in SVIX’s case are the very liquid first- and second-month VIX futures.

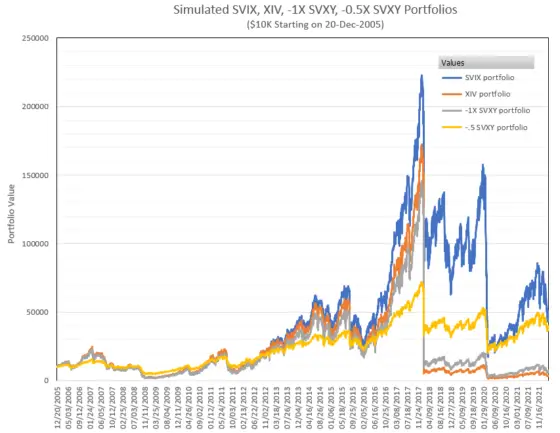

How Would SVIX Have Performed Relative to -1X and -0.5X SVXY?

- The chart below compares simulation results for SVIX with actual and simulated values for XIV and the two different leverage levels for SVXY. Before February 28th, 2018 SVXY’s goal was -1X leverage and the leverage dropped to -0.5X from then on. The -1X values for SVXY after the 28th are simulated values, as are the -0.5X values before the leverage adjustment date. XIV was terminated in February 2018, my simulation shows how it would have performed after that.

- While the SVIX simulation results are slightly better than XIV and -1X SVXY from the end of 2005 through January 2018, SVIX dropped much less than XIV and -1X SVXY on February 5th, 2018 because the worst of the decline occurred after the 4 PM close time of SVIX. That event is often referred to as “Volmageddon.”

Conclusions

- SVIX is a product intended for sophisticated investors and should not be viewed as a “buy and hold” investment.

- SVIX’s use of the SHORTVOL index and its structural limits on market volume participation will likely reduce its vulnerability to liquidity disruptions such as the 5-Feb-2018 volatility event that killed XIV and caused ProShares to reduce SVXY’s leverage.

- SVIX will still experience dramatic drawdowns when volatility spikes.

- In my opinion, SVIX is best used when the VIX Futures’ term structure is in contango and its investors have a plan to exit their position when the market is nervous (e.g., a VIX/VIX3M ratio greater than 0.95) or protective options strategies are in place to handle a volatility spike.

For more information:

Hi Vance,

I just saw it on August 5th (which day SVIX drops a lot). SVIX holds a VIX option on September @$45. but now (August 20th), it holds a VIX option on September 18th @$28 .

do you know what’s the rule for SVIX to choose an option?

thanks

Hi Sherman, I’m pretty sure there is not a fixed rule book for the VIX options. During quieter times they were only rolling them once a month. After/during 5-Aug-2024 they were shifting the positions every day. To my eye, the actions seem to those of an experienced trader. Overall I think the strategy is to hold a large enough position to give them significant buffering on a really bad volatility spike.

Best Regards, Vance

If it was holding at C$28 on August 5th, it wouldn’t have dropped so much that day. The gap between C$45 and C$28 is pretty big.

Thanks for the reply Vance..but still,why is it when the vix goes up 4% svix goes down 2% and vise/versa..what am I missing here ?…does it have anything to do with SVIX selling those calls a month or two earlier and that option premium cushions SVIX’s price drop/gain ?

still not clear..

thank you

Thanks for the reply Vance..but still,why is it when the vix goes up 4% svix goes down 2% and vise/versa..what am I missing here ?…does it have anything to do with SVIX selling those calls a month or two earlier and that option premium cushions SVIX’s price drop/gain ?

still not clear..

thank you

Hello Vance..

I’m not 100% sure but I think that your SVIX simulation chart could be wrong..SVIX goes up or down 50% of VIX’s daily percentage move,does your chart move SVIX’s 50% or 100% of the VIX’s percentage daily move ?

This would make a HUGE difference….According to your chart In FEB 2020 SVIX dropped about 90%/95% instead of 40%/45%…

Can you please double check it….because if you made an honest mistake and traders look at your chart they will stay away from SVIX for the wrong reasons..

Thanks buddy.

Hello Cyrus,

My calculations are correct. As noted in the prospectus https://www.volatilityshares.com/svix/prospectus

“SVIX seeks daily investment results, before fees and expenses, that correspond to the performance of the Short VIX Futures Index (the “Short Index”) for a single day, not for any other period.” This Short VIX Futures index is also known as “SHORTVOL”.

Also from the prospectus

“As such, SVIX can be expected to perform very differently from the inverse (-1x) of the performance of the VIX over any period, and UVIX can be expected to perform very differently from twice (2x) of the performance of the VIX over any period.

Vance

Hi Vance,

thank you for your work. I just noticed that SVIX holds some Vix call options now. I know it’s just for hedge the Vix super jump. Can you calculate how this vix call option can help in what worst situation? I mean what is the max drawdown for SVIX in the worst situation (like -70% r -80%)?

thanks ahead

Hi Sherman,

I looked at this a while back. The notional value of the calls runs around 30% of the assets under management, so it doesn’t provide guaranteed protection against go to zero scenario. Since the upward moves of the VIX futures are not constrained, unless you had 100% notional exposure with the calls a full wipeout is possible. Of course, the calls would likely help a lot during a vol spike because not only would the value of the calls go up with the value of the corresponding future, the implied volatility of the calls would also go up a bunch. So realistically your -70% to -80% number is probably a good guess for a volmageddon style event. I’ll probably do a post where I get more analytical about it, but there are a lot of moving parts, and the next major vol spike will be different from all the previous ones…

Vance

Can you comment on the role of options in the SVIX holdings?

Hi DR,

My opinion is that these options are intended to mitigate the effects on SVIX of a major volatility spike. On 5-Feb-2018 VIX futures almost doubled, an unprecedented event, and as a result essentially zero’d out the -1X leveraged XIV and SVXY. ETFs and Stocks can’t go below zero, but a short position in VIX futures, held by the ETF issuers and their brokers has no limit to its losses. By adding long VIX options to its holdings the dynamics of a large VIX futures spike would be considerably easier to manage. Not only would the VIX calls approach their strike prices, their implied volatility, which directly impacts their premium would skyrocket. Holding these calls would significantly dampen the losses SVIX’s holding, reducing the pressure to close out short positions–likely at the worst possible time. — Vance

This is a great comment… didn’t see it before my post. Sounds like the VIX position could dampen the blow in another volmageddon. Thank you!

Hi Vance,

Thank you very much for sharing your work.

Quick question please re the behaviour on the 5th of February 2018: I understand Svix wouldn’t have dropped as much as XIV/svxy on the day because of the end of day data however the product should have dropped the day after because after all it is short vix futures and those futures haven’t come off the day after at all if am correct?

Thank you very much in advance

Hi MP,

The vix futures didn’t rise much on the 6th. XIV’s value was driven by the value of the futures at settlement on the 5th, which was much higher than what it was at 4pm that day. SVIX’s effective value would have dropped dramatically during that feb 5th after market period, but would have opened on the 6th not far from its 5th close price. In the weeks that followed the VIX futures did go up some, but the low for SVIX during that period was only around $25, from a 6th Feb price of ~$30. –Vance

Thank you very much for your work,

Two questions:

I have noticed the NAV “sometimes” doesnt aling with the formula = net assets / outstanding shares. most of the time is 1% error But it can go +/-5 , why is this happening. Is anything else in the formula missing? or liabilities not published? or anything missing here?

And how do they (Proshares) address this phenomenon with creation and redemption? if its significant > -/+5, would affect the price?

thank yo very much

Hi Jerry, I’d have to see an example to explain this. The picture is complicated somewhat by how the ETF issuer handles fees and operating expenses. Those are usually subtracted from the fund’s assets on a daily basis. If the fund has borrowed money that might enter in too. I don’t know if you used official NAV numbers reported by the funds, or the day close value. Sometimes these numbers differ by a significant amount.