We don’t have good metaphors to help us understand the short-selling of equities. It’s easy to understand a straight “long” investment. For example, planting a garden is a reasonable analogy—it involves buying seeds, planting them, and in due time there is a payoff—or not.

But in real life people rarely borrow something, immediately sell it, and hope to buy it back at a cheaper price. Since we aren’t familiar with selling short many of its characteristics are counterintuitive.

Below I’ve listed some common questions and answers—hopefully, they’ll make short selling a little easier to understand.

Can I short securities in my IRA?

- No. IRS rules prevent borrowing within an IRA account—this rules out borrowing stock, the first step in a short sale. Buying inverse exchange-traded funds like SDS and SVXY is usually allowed, but your broker may require some extra paperwork. For more on IRAs see “15 Questions About Trading in an IRA”.

What happens if I’m short a security when it goes ex-dividend?

- You owe the dividend. Your broker will deduct the dividend amount from your account on the distribution date. For more on dividends see “10 Questions About Dividends”.

My short sale won’t go through because my broker says shares aren’t available to borrow. What should I do?

- Call your broker. Sometimes shares are available to borrow if you are willing to pay an additional fee—which can be relatively small (e.g., 7% per year).

- Consider using options instead, being long puts can give you a chance to profit if the security drops—with a fixed limited risk if you’re wrong. Unfortunately, options have expiration dates, a premium price, and sensitivity to volatility levels. If you have approval to sell naked calls you can create a synthetic short (long puts, short calls at the same strike price) that closely models a short position.

- Talk to other brokers. Some specialize in meeting the needs of short sellers.

- Look to see if there are equivalent inverse exchange-traded funds or notes available. See below for a discussion on inverse funds.

What is a short squeeze? Should I worry about it?

- A short squeeze can occur if the security has a relatively restricted supply of shares. If shareowners are holding tight (e.g., enjoying a recent run-up in the stock), then short sellers can get into a desperate situation with each other— bidding up the price of the stock trying to close out their positions and stem their losses.

- If you are thinking of shorting a stock, you should check the float, a measure of share availability, and the short interest. ShortSqueeze.com is an example website that provides that information.

- Properly functioning exchange-traded funds and notes are not susceptible to a classic short squeeze because they can routinely create shares if the security starts trading at a premium to the index it tracks. For more see “If There’s Liquidity It’s Not A Short Squeeze”

What does it mean that the shares I borrow can be recalled at any time?

- In a standard short selling arrangement, the loaner of the shares you borrowed can recall their shares at any point—for example, they might want to sell out their position. In practice this is rare, and the solution is straightforward—buy shares on the market to close out your position. Your broker will then return the shares to the lender. At that point. you can re-enter the position if you want to.

What is a margin call?

- When you sell short your broker will require you to have extra funds set aside in your margin account in case your short sale position starts losing money. Your broker will require that you always have enough funds in your account to close out your position. A margin call is a notification that you either need to add cash to your account, or cover some of your short position to reduce your exposure. If you don’t act, your broker will reduce your short position by buying back some of the security.

What are the trade-offs between short selling and buying a resetting inverse exchange-traded fund/note (ETF/ETN) on the same security?

- The advantages of a short position are:

- No path dependency—the value of an inverse fund is dependent on how it gets to a certain value. For example big up and down moves, even if they cancel out will erode the value of an inverse fund. This can be a big deal.

- The advantages of an inverse ETF/ETN are:

- Constant leverage, the daily percentage moves will closely track the opposite percentage moves of the underlying security. Most inverse funds will rebalance daily to keep their leverage consistent.

- Potential gains greater than 100%. The resetting process of these funds enables them to avoid the 100% gain limitation of a short sale. For example, ProShare’s -1X SVXY (now -0.5X leveraged) increased from a split-adjusted $5 per share to $130 in late 2017 (and then crashed to $9 on February 5th, 2018).

- Avoids the issues of trying to borrow shares, borrow costs, recall of shares, and margin calls (unless the shares were bought on margin)

- Your maximum loss is limited to your initial investment. With short positions your losses can be much larger than your initial position.

- Avoids the risk of the issuer of a long fund deciding to halt share creations. If this happens it breaks the control process that is used to keep an ETP trading close to it’s Indicative Value. Without this control process the price of the long fund can soar, generating heavy losses for the shorts.

How do you measure the returns on a short sale?

- For a regular long investment we use the initial cash outlay as our basis, and we divide the final result by that basis (and subtract one) to get percentage returns. However, in a short sale there is no initial cash outlay, no investment with which to compute the ROI.

- The best solution I’ve found is detailed in this paper. They use an internal rate of return approach. The key formula is:

Return = (Initial Cash flow + Final Cash flow) / Initial Cash flowSo for example, if I short 100 shares of XYZ corp at $10, I will see $1000 deposited in my margin account. If I close the position after the stock climbs to $11 my percentage loss is:

(1000-1100)/1000 = -0.1 A 10% loss.

What is the maximum percentage gain possible on a short sale?

- Unlike a long position, the maximum profit on a short sale is limited. The best case is when the stock you shorted becomes worthless. The final cash flow in that case would be zero. The return would be:

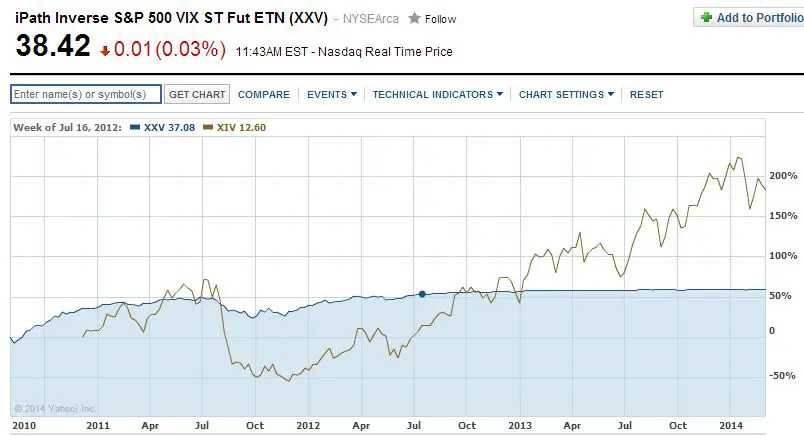

(Initial Cash flow + 0) / Initial Cash flow = 1 A 100% gain. - Barclays’ XXV fund (terminated August 2017) was essentially a true short (not a rebalanced inverse fund) of VXX that was initiated July 16th, 2010. As of March 2014, VXX had decreased a factor 40 since that date (split-adjusted 1751 to 43.24), but XXV had increased less than a factor of 2—from 20 to 38.42. The chart below compares XXV’s performance to XIV, an inverse, daily resetting ETN.

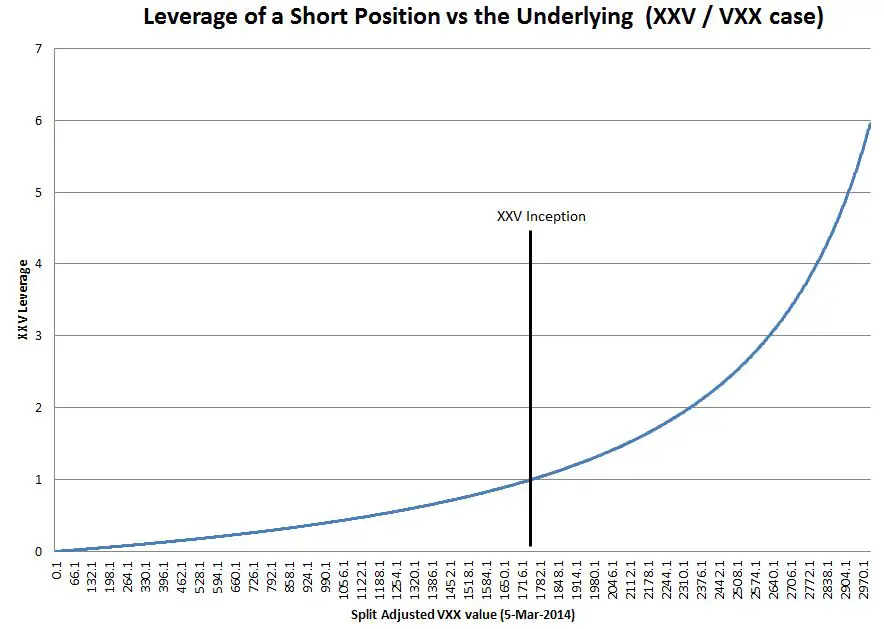

What’s the leverage of a short sale position?

- For a standard long position, the leverage is always one; if the stock goes up 10% your position goes up 10% in value. For a short position the leverage is variable, ranging from near zero to very high.

- At initiation, a short position has a leverage factor of one, but that leverage changes as soon as the price of the security changes—and not in the short seller’s favor. If the security increases in value above your sale point the leverage increases above one, below it drops under one.

- For example, assume you sold short at $10, and the security is now at $12. An additional +10% move to 13.2 would result in a -12% return—a leverage factor of 1.2

(1000-1200) / 1000 = -.2 (-20%) 1000-1320 / 1000 = -.32 (-32) - Conversely, if you sold short at $10 and the security is at $8 an additional 10% drop to $7.2 would only net a 8% return for you—a leverage factor of 0.8

(1000-800)/1000 = .2 (20%) (1000-720)/ 1000 = .28 (28%) - The chart below shows the changes in short position leverage (XXV in this case) as the underlying (VXX) moves

Consider everything you said in this article, how safe is to your opinion this scenario:

$1,000,000 account invested 20% ($200,000) in TVIX at it its lowest point.

as it wear out always and some profit taking always maintain 20% of the value of the account.

When it goes against you, stay put and wait.

TD holds 30% reserve so I actually have to deposit $1,300k.

Do you think it will work (short of the end of the world scenario)?

Hi Gary,

For starters, please read https://www.sixfigureinvesting.com/2016/10/is-shorting-uvxy-tvix-vxx-the-perfect-trade/ Being at year 11 of a bull market I think any short seller, especially of vol products needs to have an active plan for handling a big correction / bear market (not just end of the world). Just staying put is not realistic/catastrophic if the underlying goes up 10X, like TVIX would have if it had been trading in 2008/2009. Buying OTM calls in VXX or UVXY is a potential way to do that.

Vance

Wow was this comment ever prescient!

Hello,

I can’t even short UVXY for 10 share, IB said that “There is insufficient UVXY available for short sale”, what’s that mean? the volume is already more than 5 millions shares…

Thanks

Hi Vance,

Thanks for the great post. Question about the leverage on the short trades. If I short 100 VXX @ $10 = $1000, and the market spikes up 500%, then I’d be -$5000, correct?

In theory I could just hold that until it reaches my target price, provided that I have enough to not get a margin call and expected this might happen eventually.

And to avoid getting a margin call, I can factor in the maximum total spike, trough to peak during 08. Is the logic correct here?

Hi hb7o9, Your math is correct. You’re also correct in that if you have enough margin (and the ability to hang in there when everyone is saying the sky is falling) you can ride out the storm and eventually get back to profitability. Another approach would be to buy enough out of the money VXX calls to limit your draw down to a more manageable level.

Thank you sir! I love your blog.

Hi Vance I have 2 questions. The first is I want to short vxx but the funds are in a retirement account and I’m not fond of the skew for DITM puts. Other than having to accept the offer price (before expiration) due to liquidity why wouldn’t shorting a SSF contract on VXX be practical?

My second question is why are the daily returns between ziv and vxz so large? IB has vxz up 1.1% but ziv is down 1.9% I thought they would mirror each other a little better since to my knowledge they are based on the same futures contracts.

thanks

Hi Hans,

If your IRA allows you to trade VIX futures then that also works to go short volatility-you just have to manage the expiration.. Even if they allow futures I suspect they will require a spread position. You could also buy XIV to go short on volatility–historically it’s behavior is equivalent to short VXX in the short term and better than a short long term.

Regarding the daily returns on ZIV vs VXZ you have to use indicative values ($ZIV.IV on Schwab) to do the comparison, otherwise you’re just seeing last trade info. They track very closely at a daily level. For more see https://www.sixfigureinvesting.com/2013/03/is-etf-etn-broken/

Best Regards,

Vance