Why is mid or medium-term volatility defined as being 4 to 7 months out?

- In January 2009 Barclays introduced VXZ, the first medium-term volatility Exchange Traded Product (ETP). Its tracking index (SPVXMP) relies on 4 to 7-month VIX futures. I suspect that range was selected because historically (2004 through 2008) the term structure on the 4th through 7th-month VIX futures was relatively flat but still tracked general volatility trends.

- By using the 4 to 7-month range Barclays could minimize transaction costs by holding futures for a full 3 months when it came to implementing VXZ’s hedging strategies.

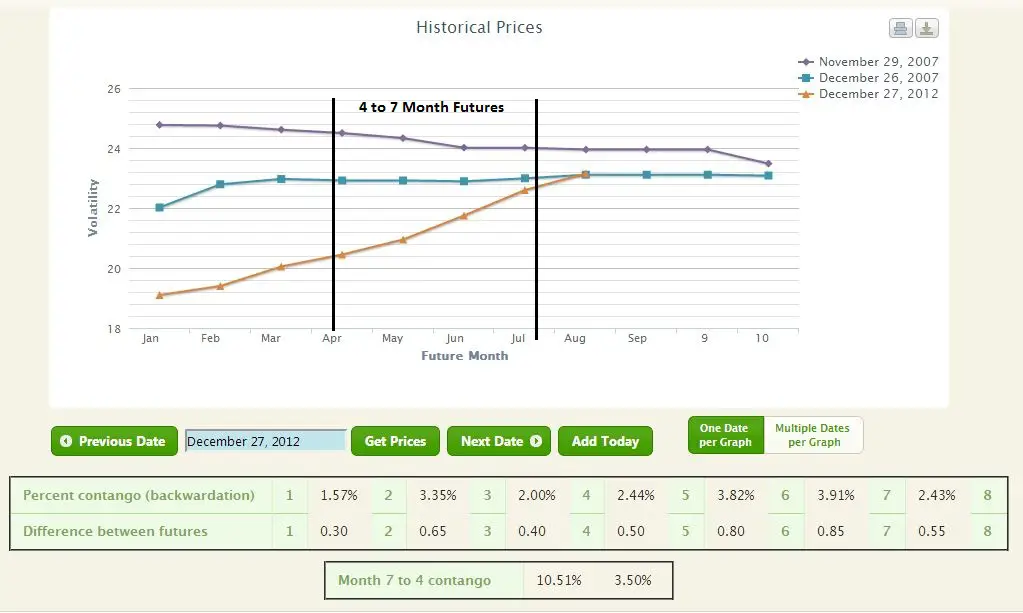

- The chart below from VIX central shows the VIX futures term structure on 3 different dates:

How does the mid-term rolling volatility index(SPVXMP) work?

- At the end of every trading day the index models the selling of a portion of the 4-month futures that it holds and uses the proceeds to buy an equivalent dollar amount of 7 month futures. The process sells the last of the 4-month futures the evening before the nearest (1 month) futures expire.

Can I invest in mid-term volatility?

- There are 3 ETPs that hold at least some of their assets in mid-term VIX Futures. Specifically:

- 1X long: VXZ, VIXM (ETF)

- Hybrids that hold a portion of their assets in mid-term futures: XVZ

- See Volatility Tickers for the full list of USA volatility related ETPs, their websites, prospectus, etc.

- For a mid-term volatility investment strategy that utilizes the VIX for timing see Taming Inverse Volatility with a Simple Ratio.

What does it mean when mid-term volatility futures are in contango?

- Contango is a futures market term signifying that contracts with more time until expiration are more expensive than shorter-term contracts. In commodities markets (e.g., natural gas) this is the typical state if supply and demand are in balance and the product has carry costs (e.g., storage).

- When futures markets are in contango it’s expensive to hold (be long) futures because the contracts are decreasing in value over time. Of course, if the underlying commodity/index that the future is based on increases enough it will compensate for those losses.

How often are mid-term VIX Futures in contango?

- Historically around 75% of the time—typically when the equities markets are bullish or trading within a range

How do you compute contango on mid-term volatility?

- The total amount of contango is just the percentage difference between the 7th-month and 4th-month futures’ price (e.g, (M7-M4)/M4). Divide this result by 3 to get an estimate of how much the value of a medium term position in volatility will decrease in a month due to contango.

What happens if medium term VIX futures have a negative slope (longer term contracts cheaper then shorter term)?

- This situation is called backwardation. It happens when the markets are very fearful. In this case, the rolling index will tend to increase in value because the contracts get more valuable as they get closer to expiration.

- A contango calculation in this case will yield a negative number

How volatile is medium term volatility compared to short term (1 to 2 months)?

- Medium-term volatility tends to experience about half the volatility of short term. In 2012 the annualized volatility was around 35%, compared to 70% for the short term rolling indexes.

Has the general behavior of mid-term VIX futures been stable?

- For the first 6 years of VIX futures trading (starting in 2004) the mid-term futures term structure tended to be quite flat during quiet times. However, starting in late 2009 the typical structure has shifted to a fairly steep structure, with the 4th month futures trading for significantly less than the longer-dated futures.

What are the advantages/disadvantages of investing in mid-term volatility?

- Disadvantages

- Mid-term volatility moves much slower than the 1 to 2-month short term volatility measures. If you are trying to catch the full impact of a volatility spike mid-term is not for you

- Advantages

- If you want to be short volatility, the medium-term investments are not as scary. An overnight volatility event (e.g., earthquake, terrorist event) will not move the mid-term indexes near as much as the short term.

- The contango losses in the rolling indexes are lower than the short term indexes, lowering the costs of holding a long volatility position. However, the contango losses in medium term volatility sometimes increase to painful levels—often running in the 3 to 5% per month level.

http://vixcentral.com/historical/?days=30

The past history page that I could see on this page is no longer displayed. Is it under maintenance?

Seems to be working now. By the way, not my website.

RB – the 2nd % is the monthly drop due to contango, the first number / 3

The month 7 to month 4 grid details show two percentage numbers.

The first percentage number is the level of contango.

What does the second percentage number represent?

Great article, Vance!

I just want to make sure…you said that 75% of the time, VIX futures are in contango. Is it from 2004-now? Or 2009-now?

Because you wrote that between 2004-2009, mid term VIX futures are relatively flat. If it’s flat, than can we call it contango?

Hi Hendra, The 75% number is from 2004 on. The mid-term contango in 2004-2006 was in the 1% to 2% level, which is pretty flat, but still contangoed.

— Vance