The short-term Volatility ETPs hold a mix of the two nearest-to-expiration VIX futures. The ETPs are either long both of those (e.g., VXX, UVXY, UVIX, VIXY) or short both of those (SVIX, SVXY). If the VIX futures term structure is in contango, with prices increasing with time, then the tendency will be for both futures to drop in value on a daily basis–so a long ETP will tend to drop in value and the short ETPs will increase in value.

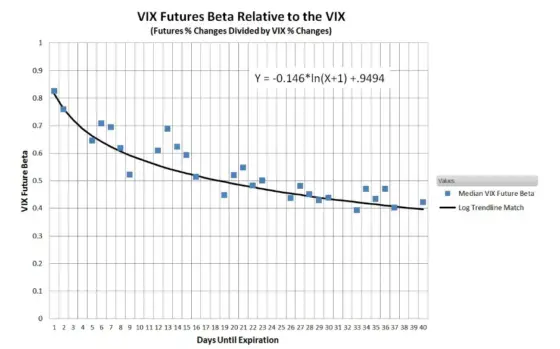

The rate at which VIX Futures converge to spot VIX varies, and their tracking to the VIX depends on how much time the VIX future has before expiration. Near expiration, a VIX future will converge rapidly to the VIX, and will track changes to the VIX at pretty much a 1:1 ratio. A VIX future with 3 months to expiration is much less correlated with the VIX value.

Complicating this whole situation is the fact that the ETP’s change their mix of VIX futures on a trading daily basis to shift out of the next-to-expire future into one with more time until expiration. Contrary to most people’s intuition, this roll process is economically neutral, it’s like changing two nickels for a dime; there’s no net loss (see The Cost of Contango)

With leveraged ETPs like UVIX and SVIX, things are further complicated by their need to rebalance their assets daily so that their next-day performance will match their leverage goal. Over time this rebalancing process results in volatility drag that significantly erodes the price of the leveraged ETPs, but in a strongly trending market results in leveraged ETPs outperforming their leverage factor.

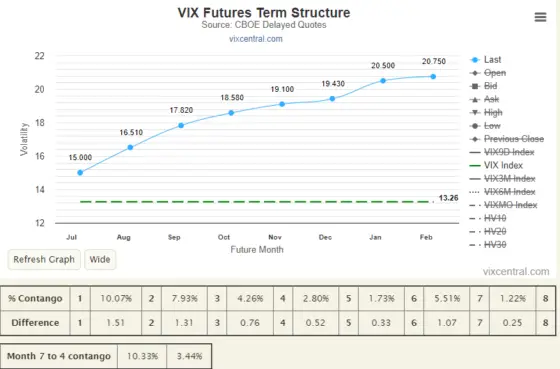

Measures of the VIX term structure, e.g., VIX3M/VIX or VIX90/VIX30 give a qualitative feel for how the ETP prices are going to trend, but as you can see, they are fairly distant from what is really going on.

Hi Vance,

Do you have any idea about why SVIX is now holding OTM call option on the VIX? I assume it’s required by the clearing house because obviously it dislocates it from mirroring the SHORTVOL index. But presumably with VIX quite low right now, the custodian/clearing for volatility shares want them to hedge against a 100% move in the VIX (which wouldn’t really result in a 100% upward move in futures anyway, historically) and is FORCING them to do that. But I thought that with how SVIX and SHORTVOL was designed that it was not really possible for have a 2018 type volmageddon anyway due to it not rebalancing. So theoretically only if VIX futures went up 100% within 30 days (has that ever happened?) that’s when SHORTVOL could fall to 0?

Hi Edgar,

SVIX/ShortVol is not immune to a Volmageddon event, it lowers the risk profile considerably, by spreading out its rebalancing and limiting its volume of sales, deferring rebalancing if needed, but there’s nothing structural that prevents the VIX futures that SVIX shorts from more than doubling in a day. Shortvol could go to zero in a single day, multiple-day moves are not as important because its rebalancing tends to mute the impact of a market trending up in volatility.

I suspect that Volatility Shares wasn’t forced to do this, but the FCMs doing the actual buying/selling of futures would likely make it expensive for them if they didn’t implement something like this. I think that once SVIX got up into the $100M AUM area this becameimportant. I plan to do a blog post on this, doing some simulations, but my intuition is that these call positions, while not even close to fully hedging big moves, would significantly buffer the moves during a very volatile day. Since the VIX itself and the IV on VIX calls would both spike on a bad day there is more leverage there that one might guess. The call position could very well prevent the situation where the FCM felt they had to protect themselves by covering some of their short positions. This would likely happen at the worst possible time, so having something in the portfolio going up dramatically at the same time would likely reduce the need to make quick moves, which is typically the worst time to be trying to cover a short position. — Vance

Hi Vance

Do you have an article or any wisdom regarding Vix seasonality .

There were lately charts published showing as if from early July Vix average value increase significantly until year end