The Cboe is just dribbling out information so far (30-April-2023), on the new one Day VIX (VIX1D), but so far the evidence supports the following guesses:

- VIX1D quotes, download data for the previous 3 months, chart data back to May 2022 are available on Cboe’s Global Index site. Beware, the open/high/low data is the same for all days until the beginning of April. It appears it will be a while before we can get a statistical feel for things like day of week close to open moves.

- The VIX1D is a relatively straightforward extension of the current VIX methodology down to one day, the details are given in this VIX1D whitepaper.

- The real-time value of the VIX1D will represent a dynamic mix of the SPX options expiring today and of the ones expiring the next trading day. By the end of the trading day, the VIX1D will be totally driven by the price of the SPX options expiring the next trading day, which could be multiple calendar days hence (e.g. weekends + holidays).

- VIX1D will be very sensitive to Known-Unknown event risk, where the timing of an event (e.g., Fed report, Election date) is known but the outcome is not. When that event has the potential to move the market, SPX option prices, in particular options expiring soonest after the announcement, reflect the magnitude of the likely move, which in turn impacts the value of the VIX1D index.

- Calendar effects will be present in the VIX1D, which are described in more detail in, No the VIX is Not Broken. Briefly, the VIX calculation needs a normalization calculation to standardize the volatility metric to be an annualized number, but things like weekends and holidays can create unreal artifacts in the index. For example, the VIX and the VIX9D typically have a significant jump on Monday mornings, which is not present in the tradeable VIX futures. With VIX1D this weekend effect will move to Fridays.

- Two important tweaks to the VIX methodology described in the VIX1D whitepaper to make it more suitable for the one-day time duration are:

- The use of “business” time” vs the standard calendar time for the variance interpolation between today’s and tomorrow’s variance calculation during regular trading hours. This will dampen down some of the weirder effects. For a deep dive into the variance interpolation calculation, you can read Calculating the VIX-the Easy Part, where I discuss/document this process for the standard VIX index.

- The methodology also calls for ignoring the changes in the current day’s results after 3PM ET, freezing the value at the 3PM level. This prevents last-minute option price funnies common right before market close from unduly influencing the VIX1D’s level.

- With the explosion of 0DTE option volumes, it seems likely that the Cboe would want to get VIX options into the expirations every day game, however using its current processes, VIX options have a 30-day horizon, which react slower than true ODTE options which closely track the current “spot” price of their underlying security.

- One possible goal of introducing the VIX1D would be to facilitate the introduction of everyday expiring VIX options with a one-day horizon. Current monthly and weekly VIX options have a 30-day horizon. To accomplish this the Cboe would have to create a variation on the current auction process, called the Special Opening Quotation (SOQ) to generate the settlement price, because the current one, running typically on Wednesday mornings, settles to SPX options with 30 days until expiration. Currently, VIX options typically only expire on Wednesday mornings, and have a 30-day horizon.

- When/if VIX everyday expiring options come out, they might take the opportunity to change the expiration to the market close, when virtually all other options expire. The current AM expiration is just an artifact of the initial SPX options that expired in the morning (AM). If they did create a new SOC then running it at market close would be attractive, more intuitive, aligns better with other option products, and avoid the sometimes chaotic environment at market open.

- It’s not likely that the Cboe will introduce VIX daily expiring VIX futures any time soon.

- If the CBOE is just adding a new VIX index, then they’ve created a very quirky one. One that virtually no one will really understand, that occasionally generates very high, untradeable values as clickbait.

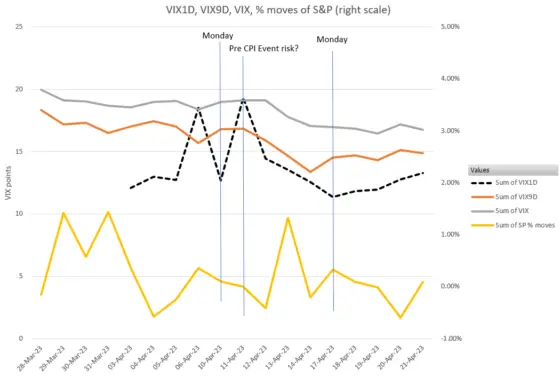

So far, the Cboe has released 1 year of backtest data for the VIX1D (VIX1D dashboard), but even that little snippet of data confirms that this extension to the VIX family will expand its general ability to confuse people. The chart below compares 14 days of VIX1D (dotted black line) with VIX9D, VIX, and the daily percentage moves of S&P500 (scale on right).

The major two spikes, one on April 6th, and another on April 11th, immediately stand out. Not only do the other indexes not have these big spikes, the VIX1D spikes don’t align with the general S&P 500 market action. Neither of these spikes are reflecting the “true” volatility of the market that day (whatever the hell that is). The first spike is likely the weekend effect I mentioned earlier, and the second spike on April 11th is probably an event-driven spike driven by the April CPI announcement on the 12th.

Regarding the introduction of everyday expiring VIX futures, I think this is unlikely. The Cboe did create weekly expiring VIX Futures around the time they created weekly expiring VIX options, but they have never had much volume, their volumes are much lower than the monthly expiring VIX future. With the liquid monthly VIX futures, VIX options, and VIX-based Exchange Traded Products (e.g, VXX, VIXY, UVXY, UVIX) and their options I think investors and market makers don’t need/want another tenor of VIX futures. Unlike Americal style options, VIX options are European style (not early exercisable) and cash-settled, so they don’t require a physical security to assign to.

The Cboe recently (20-Mar-2023) updated their Special Opening Quotation (SOQ) process in the VIX white paper. This auction, which currently occurs most Wednesday mornings after market open is the mechanism that establishes the settlement price of VIX options and futures that expire on that day. One of the changes in the SOQ process is that the Cboe now specifies the specific SPX option put and call strikes that will be included in the auction. This removes one source of uncertainty in the SOQ auction process that was exploited at least once in the past, in an attempt to game the VIX settlement price. If the Cboe does introduce everyday VIX options with one-day horizons a modified SOC process would need to be created that occurred every trading day to establish the settlement price. A robust final value process for determining the expiration price is very important.

If the Cboe does introduce everyday expiring VIX options, one consistent confusion factor will likely be amplified. For most options, e.g., SPY, Apple, the current stock price is a reasonable proxy for the underlying security that the option is tracking. In reality, options track what’s called the forward of the underlying security, which captures things like interest rate effects. For VIX options the standard VIX indexes are essentially never a good estimate of what the options are tracking. For VIX options expiring at the same time as a monthly future, that future is a good estimate of the forward price, but for something like a VIX option expiring next Thursday there’s nothing reliable. If you just use the current VIX values you could be way off. The best estimate of the forward value for your option is the level where the put and the call of that expiration have the lowest prices. The Greeks that brokers display for these options are often calculated using the wrong underlying, so they can be way off.

In conclusion, these are all preliminary guesses, we will know more as we get more details on the new VIX1D index.

Great explanation. Would it be possible to get a forward underlying for a VIX option expiring “next Thursday” or any other day with an average price between spot VIX and the nearest expiring VIX future contract price weighted to next Thursday? Thanks.

Hi Nathan,

This isn’t an area I’m super confident about. The VIX futures price for a specific expiration is a pretty good estimate for the forward price for that date. I would expect VIX options expiring on that same data to be priced off that value. To interpolate between that price and the spot to get an intermediate forward price you’d have to recognize first of all that volatility doesn’t interpolate linearly with time, to address that in the VIX interpolation they use variance (volatility squared), which theoretically does scale linearly with time, and then they convert the resultant variance number back to volatility. This might give a false sense of correctness however because the front part of the VIX future term structure can also be strongly influenced by event risk, and market conditions, which at times overwhelms the normal, volatility increasing with the square root of time effect.

The other approach would be to look at the price of a synthetic long position, created by buying the call and selling the put for the expiration you’re interested in at the same strike. The cost of the synthetic plus the strike price is probably pretty close to the forward price.

Best Regards,

Vance

Hi Vince,

I went with the second option as the link still auto populates the shopping cart with one of your free downloads instead. very odd. in any case i sent you the money vs paypal. thanks!

Justin

Vince,

I’m trying to purchase the $29 UVXY historical backtest but your site doesn’t seem to be working, as it keeps populating the cart with a different (free product). please advise. thanks!

Hi Justin,

My apologies for the problem. I’m not able to recreate the problem from my end. You might try this direct link https://www.sixfigureinvesting.com/product/proshares-1-5x-uvxy-backtest/ Otherwise, if you send $29 to Paypal at [email protected] I will email the spreadsheet to you directly. Best Regards, Vance