Volatility Shares’ next UVIX reverse split, will be a 1:10 reverse split, and will occur 15-Jan-2025 (press release). Since its inception in March 2022, UVIX’s decay rate has averaged around 20% per month.

Some investors anticipate significant price moves in UVIX motivated by a reverse split. I’m not in that camp. UVIX’s price is tied to VIX futures’ price, which couldn’t care less about UVIX’s share price. A long time ago it was common for stocks to have sizeable run-ups motivated by upcoming splits (not reverse splits). But a split does not provide any economic edge or penalty, at least with the shares themselves, and I think this strategy stopped working a long time ago. At best, forward stock splits are a momentum indicator.

Reverse splits do have some significant second-order effects on options, which I talk about later in this post.

Volatility Share’s 2X leveraged short-term volatility ETP, UVIX, must frequently reverse split to keep its prices in a reasonable trading range—otherwise, its long-term share would trend zero. For example, a share of UVXY, a similar ETF, purchased for $40 at the fund’s inception in 2011 would now be worth less than 0.0001 cents.

The reason for this rapid erosion of value can be found in “How Does UVIX Work?” Lacking bear markets, these funds are ravaged by contango at rates that vary between 50% and 85% per year. Monthly decay rates run in the 20% range.

From my simulations, 2X leveraged volatility funds will reverse split about every 8 to 22 months.

UVIX Reverse Split History

| Event | Dates | Split Ratio | Inception / close price right before reverse split (split adjusted) | Months since inception /last split | Average Monthly Decay Rate since inception/last reverse split |

| Inception | 30-Mar-2022 | $15 | -16% Lifetime | ||

| 1st Rev. Split | 25-Jan-2023 | 1:5 | 3.89 | 10 | -12.5% |

| 2nd Rev. Split | 11-Oct-2023 | 1:10 | 3.88 | 8 | -20% |

| 3rd Rev. Split | 15-Jan-2025 | 1:10 | ~ 3 (est) | 15 | -18% |

If you hold shares of UVIX there isn’t anything to worry about when it reverse splits. The value of your investment stays the same through the reverse split process, however, your broker may charge some fees, e.g., $20 “Reorg Fee”. You just have 5X fewer shares that are worth 5X more each (assuming a reverse split ratio of 1:5). If your share holdings are not a multiple of five, say 213 shares, you will get 42 reverse adjusted shares and a cash payout for the 3 remaining pre-split shares.

If you are short UVIX, same story, no material impact.

In theory, if you’re holding UVIX options (long or short) when the reverse split occurs there’s no material impact, There will be set of spilt adjusted option chains generated that will show pricing on your options, and those prices should have continuity with the pre-split values. However, In practice there are issues.

- The split-adjusted chains can take up to a week to start trading again, which if the timing is bad could be a big deal.

- The bid/ask spreads tend to widen out on the split-adjusted option series. The option market makers attention has shifted to the new option series created after the split, so they aren’t competing for business on the adjusted options. I’ve seen zero bids on options that are clearly worth something, and outrageous asks. If this happens, don’t freak out, if you want to close the positions, you should still be able to get fills via limit orders between the bid/ask price. You can use an option calculator + prices on the new option series to figure out an appropriate price. If you’re long, you also have the capability to exercise your options, and sell the underlying to capture any intrinsic value. Lack of volume or open interest doesn’t mean there isn’t liquidity, if your position still has significant value, you can still close out your position to capture most of that value, it will just require more effort on your part.

- If your option positions are being used to hedge a position in the underlying, e.g., long calls to hedge a short UVIX position, then there is a risk that your broker’s margin calculations will be disrupted by the reverse split on the options. If there are no quotes, or if your broker’s software can’t handle the non-trivial calculations associated with the adjusted option series, you might get a margin call and/or a forced close-out of your position. If you’re in a situation like this, a call to your broker before the reverse split is in order. One possible workaround, would be to shift the options to another security (e.g., VXX or $VIX ) at appropriate ratios until after the reverse split, or hedge the underlying by effectively nullifying the position (e.g., by holding the appropriate number of VXX shares) until the split has happened and the options are trading again. This strategy is sometimes called “shorting against the box”, which is a reference to when people used to hold their paper stock certificates in safety deposit boxes.

- Understanding the split-adjusted options chains likely will hurt your head. The Options Clearing Corporation adjusts for the reverse split by adjusting the number of shares per contract by the split ratio. For a 1:5 reverse split the number of shares of the underlying represented by the option contract will go from the usual 100 to 20. The option chains don’t adjust the strikes, and the underlying symbol changes to UVIX# (some number, likely one or two)—which is 20% of UVIX’s price. New options will be generated with newly reverse split UVIX as the underlying, but the old adjusted options will hang around until they expire. In general, if you’re hoping to sell your options at some point, rather than just letting them expire it’s probably a good idea to roll your options into the current series after the split. A combo order closing out the old position with an opening order in the new series with an appropriately priced limit order, is probably the best approach. Start with a price you know that’s too good to be true for you, and gradually shift it in the market maker’s favor until you get filled.

For regular, forward splits things are more straightforward —the strike price of the options is divided by the split ratio, and the number of contracts is multiplied by the split ratio. See the OCC memo on an SVXY’s 2:1 split for an example. SVXY did a 2:1 split on 14-July-17. This basic approach can’t be used on reverse splits (multiply the strike price and divide the number of contacts by the split ratio), because depending on the number of contracts held some customers would end up with fractional contracts—which is a no-go.

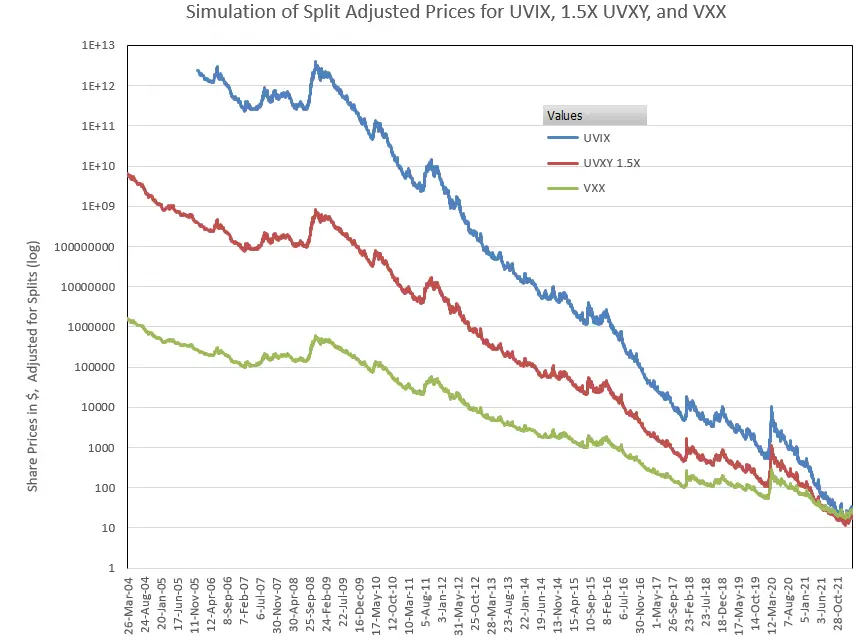

The chart below uses my simulated data to show what UVIX, 1.5X UVXY & VXX prices would have been starting in 2004

For more on UVIX see:

thanks a lot for the article. quick question how do you calculate a 20% monthly decay? how did you come up with this number? Thanks in advance.

Hi Simon, What I do is to pick a starting and ending price (adjust if necessary for stock splits/ reverse splits) and note how many periods (typically months of years) there are between those two points So pick P_start & P_stop then use the compound growth/loss formula % growth/loss = (P_stop/P_start)^(1/p) -1 where p is the number of periods between the two prices. Best Regards, Vance

Thanks for the very informative post. I honestly was not aware that there could be up to a week where the old options chains may not even trade. In my case the options I’m short are far OTM at this point, but… this is yet another item that should be included in my risk considerations!

This would be a totally separate topic, but… I’d love to know your thoughts on the Saturday expiry of options as well. People are well aware of the Friday post-market movement, but how about a Saturday morning event? I’m assuming market makers could still exercise options if they were long calls up until 11:59AM EST on Saturday. One major global event on an early Saturday, and all of a sudden, what you thought was worthless… isn’t!

Hi Lee, I’m certainly not an expert on the Saturday expiration exposure. A quick search indicates that an individual only has until 4:30 PM ET Friday to contact their broker and request that the expiring option be exercised. In addition, my understanding is that typically a broker will exercise or not exercise an option based on its price at close on the day of expiration. Now if something extraordinary happens after 4:30 on Friday night and the true expiration on Saturday morning, such as the announcement of a special dividend or company news then I suppose the market makers or brokers might be able to exercise an option that closed on Friday OTM but is now likely worth something. I vaguely remember getting a call from a broker, where the Saturday risk was a factor that I had not considered. I could certainly imagine a market maker that holds long calls or puts might be able to exercise them late Friday night or Saturday morning if it suited them. — Vance

Thanks Vance,

This is essentially my understanding as well. It would not be the average retail individual that I’d be worried about – I contacted my broker (Fidelity) and they seemed quite confident that no Retail investors would be able to make assignments on a Saturday. That’s definitively true for Fidelity customers, and they thought that to be the case for nearly all other brokerages as well.

They directed me to the Option Clearing Corporation. In looking over their info, it would seem that making an assignment on Saturday would essentially be against the rules unless it had been “booked” Friday, as the options have technically expired. However, the feeds from institutions come into them Saturday morning – that leaves a bit of room in the system for things to be potentially “gamed” – what’s to stop an institution from saying the assignment was requested on Friday, and they’re just looking for the OCC to match? Would this happen? One would hope not, but… if there was a lot of easy money on the line, I’m not certain.

I have an email into the OCC to see if they’ll shed any more light on this, but I’m not super hopeful.

No one will care about this nuance, until a 9/11 type deal happens on a Saturday morning. Then, I suppose it could become a hot topic!

Hi Lee, Thanks. Please let me know if you find out anything else. — Vance