Arbitrage processes associated with Exchange Traded Products are normally invisible to investors but are essential for ETPs to trade as they are intended. This post describes these arbitrage processes in detail and explains how they can (and have) gone wrong.

Exchange Traded Products (ETPs) enable stock-like trading of collections of securities that would be more difficult, or impossible to trade directly. For example, it’s not practical for a typical retail investor to track the moves of the S&P 500 by buying shares of all 500 individual stocks, but with ETPs (e.g., SPY, VOO, IVV) individual investors can track the moves of the S&P 500 with an annual fee of less than 0.1%

When a stock trades on an exchange, the price of the trade is a straightforward, value-based event. The seller either needs cash or has decided the stock’s price is currently too high relative to its value, while the buyer believes the current price is attractively low relative to its value. It’s different with trades of Exchange Traded Products (ETPs).

Unlike stocks, ETPs always have two prices in play, the current trading price, and the ETP’s indicative value (IV). The IV value, sometimes referred to as the indicative Net Asset Price (iNAV), is calculated one of two ways, depending on whether the ETP is an Exchange Traded Fund (ETF) or an Exchange Traded Note (ETN). An ETF holds the assets specified in its reference index, so its IV price is simply the current value of the fund’s assets divided by the shares outstanding. ETNs are less intuitive; they are legally a bond whose value tracks an index. ETN’s issuers don’t disclose what securities they are using to hedge their positions, so their IV value is computed using their reference index. For example, Barclays’ VXX ETN IV tracks the S&P Dow Jones Indices’ SPVXSTR index.

- Contents

- How Arbitrage Works With ETPs

- What Can Go Wrong?

- Conclusion

Price Tracking with ETPs

One might think that the prices ETP trade at and their IV prices would naturally stay close to each other, but they don’t. An ETP’s price, driven by imbalances between supply and demand, will often trade at prices that differ from its IV price and sometimes the difference is significant. The potential for an ETP’s trading price to drift away from the underlying asset prices is a characteristic shared with one type of mutual fund, Closed-End Funds (CEFs). However, CEFs differ from ETPs in that even when operating normally, CEFs can trade for long periods of time at large premiums or discounts relative to the assets they hold. For example, as of July 2022, Greyscale Bitcoin Trust (GTBC), a CEF, is trading at a 31% discount relative to the Bitcoins it holds.

Investors usually want an ETP or CEF share price to closely track the value of the securities they hold/reference, but in practice, the only way to achieve that is to enable arbitrage between the security and the securities it references. CEFs lack arbitrage mechanisms, but ETPs were designed from the ground up to enable arbitrage.

Arbitrage involves the simultaneous buying and selling of an asset or its equivalent in different markets to profit from price differences. For example, if gold was trading at $1700 per ounce in New York and $1800 per ounce in London you could make an instant $100 profit by buying an ounce of gold in New York and immediately selling it in London. One characteristic of arbitrage in action is that it naturally reduces any price differences in the same security trading in different markets. In the gold example, the repeated buying of gold in New York and selling it in London to take advantage of the price difference would tend to bring the price of gold up in New York, and down in London, only halting when the frictions involved (e.g., fees, commissions) ate up all the profits.

ETP issuers enable arbitrage operations on their shares by offering two services, Share Redemptions, and Share Creations. A key aspect of these services is that they only reference the ETPs shares and the underlying assets or the IV price. They are never tied to the current market price of the ETP’s shares. Because ETP arbitrage is a complex and capital-intensive operation, ETP issuers contract with institutions called “Authorized Participants” (APs) to be the only clients able to access these processes.

The share redemption service accepts ETP shares from the APs in exchange for cash at the IV price or the appropriate mix or basket of the securities specified by the ETP issuer. The share creation service takes cash or an appropriate basket of securities from the APs and gives them shares of the ETP in exchange. These services are only available for large blocks of shares, typically at least 25,000 shares.

Using these two services, APs transact arbitrage operations almost invisibly for thousands of ETPs, keeping their trade prices to their IV prices during regular trading hours. However, occasionally things break and bad things can happen. We’ll talk about the failures later, but first, we’ll discuss the ETP arbitrage processes in more detail.

When an ETP is Trading at a Discount to its IV price

If an ETP is trading sufficiently below its IV value, any trader can potentially profit from that undervalued status by buying the ETP and selling it if/when the discount to the IV price disappears. However, there are two major risks with this strategy:

- The trading price of the ETP might drop due to normal market dynamics.

- The discount between the trading price and IV price might persist or even increase.

A trader can eliminate the first risk by also shorting the appropriate securities held by the ETP. If you’re not familiar with short selling you can get more information here. There is no widely available method to eliminate the risk of the second point, that the discount of the trading relative to the IV price might not go away, and could increase and any time.

The share redemption process provides a way for APs to eliminate this second risk. When an ETF’s shares are trading at a significant discount to its IV price an AP will typically:

- Buy shares of the ETF and simultaneously sell short the appropriate quantity of the underlying securities. Since the ETF shares are trading at a discount relative to the ETF’s underlying asset value the AP will gain cash as the result of these trades.

- Arrange with the ETF issuer to do a share redemption (there are fees involved)

- At redemption, the purchased shares are transferred to the ETP issuer and the appropriate basket of securities is transferred to the AP in exchange.

- The securities transferred from the ETP issuer are used to close out the AP’s short positions

Let’s say an ETF was trading at $99/share, one percent below its $100 IV price when an AP initiates the first part of an arbitrage transaction. Ignoring commissions and fees, the AP spends $2.475 Million buying 25K shares of the ETF at the $99 price. The AP simultaneously obtains $2.5 Million by shorting the appropriate securities linked to those 25K ETF shares. The AP’s cash balance now shows a $25K gain. This profit is locked in for the AP even though the trading price, IV price, and discount will likely change before the arbitrage transactions have been completed.

Next, the AP brings the shares to the ETF issuer for redemption, let’s suppose the trading price of the ETF shares at that point has dropped 50 cents to $98.5, and the IV price has dropped $1 to $99, reducing the trade price discount relative to the IV price to 0.5%. The AP isn’t impacted by either of these price changes. The AP transfers its 25K shares to the ETP issuer, and the issuer transfers securities equivalent to the 25K ETF shares to the AP. The AP then uses those securities to close out its short positions, which then leaves them with no securities positions and a net increase of $25K in cash. The AP’s profit isn’t impacted by the drop in the value of the shares or the decrease in discount between the IV and trading prices.

Enabled by the redemption process, APs can make profitable and essentially riskless trades when an ETP is trading sufficiently below its IV price. As long as the discount is large enough to meet their profit goals, the APs will aggressively repeat these arbitrage transactions. The large purchases of ETPs shares that APs make as part of this arbitrage process naturally tend to increase share prices. By enabling APs to make low-risk profits, ETP issuers harness the AP’s essentially infinite pool of capital to buy the ETF’s shares, creating demand that tends to push an ETPs trading price back up towards its IV price.

Historically, ETP redemption processes have been very robust. The only real risk is if the issuer goes bankrupt, which as far as I know has only happened once in the USA (Lehmann Brothers 2008). Unfortunately, the process for addressing the situation when an ETP is trading at a premium relative to its IV price is more likely to break.

When an ETP is Trading at a Premium to its IV price

The AP actions required for arbitrage if an ETP is trading significantly above its IV value are essentially the mirror image of the discount case. Instead of buying ETPs shares, APs sell shares. Instead of shorting the basket, they buy the basket. Instead of redeeming shares, the APs use the ETP issuer’s share creation service.

APs have access to large amounts of cash, so buying lots of ETP shares as part of an arbitrage operation is not a problem. However, it’s a significantly more complicated proposition when APs need to sell essentially unlimited amounts of ETP shares. APs are not going to hold large positions in unhedged ETPs shares just in case they will be needed for arbitrage operations. Unlike cash, the value of ETPs shares can drop dramatically depending on market conditions—a risk that APs are not willing to take.

What APs can do proactively is build a large hedged inventory of ETPs shares. They can obtain ETPs shares at the IV price via the share creation process, and hedge that inventory by shorting the appropriate amount of the securities that underly the ETP. The net effect of these positions is that any gains/losses in the ETP shares are offset by losses/gains in the short securities. With this approach, the APs can sell shares out of their inventory as needed when the ETP is trading at a premium relative to its IV price. Unfortunately, an inventory-based strategy has two problems: uncertainty about the number of shares you’ll need to sell, and the required capital and attention needed to maintain that inventory.

Alternately, APs can skip building inventories of ETP shares and just react to ETPs shares trading at a premium above their IV prices by selling ETP shares they don’t own as part of their arbitrage trades. This short selling might involve borrowing ETP shares from other entities and then selling them. However, more likely the APs skip the borrowing part and just sell the number of shares they want to on the market, a process called naked short selling. The SEC permits some institutional players to do this, provided they arrange with other institutions to borrow the needed shares or close out the short position within a few days. Typically, APs will do the latter, closing out their short position by using the ETP issuer’s share creation process to produce the required shares.

If short selling on an ETP is not permitted or has been restricted by the Uptick rule, then APs will likely use the inventory method of obtaining ETP shares to sell when the ETP is trading at a premium relative to its IV price.

The chart below shows the trading price vs IV price for ProShares’ long volatility ETF VIXY for a year. The APs are presumably doing their arbitrage operations behind the scenes to keep the security trading close to its IV price. The chart shows that most of the time the premium/discount of the trading price to IV price was within +-0.5%, with a few excursions close to +-1% and one dip to -2.4%.

APs aren’t required to do arbitrage. They will only put on an arbitrage trade when it is possible, prudent, and profitable for them. When APs aren’t doing arbitrage operations, ETPs can trade at large premiums or discounts to their IV price. These price dislocations are often short-lived, ranging in duration from a few seconds to a few hours, but sometimes premiums are persistent, lasting months or years.

Short Term Premiums/Discounts to the IV price

While exchanges can process trades in microseconds or less, arbitrage processes are inherently slower, it’s probably at least a few seconds before APs can act to reduce price premiums or discounts. Fast, transient dislocations between the trading price of an ETP and its IV price are likely a response to one of two situations:

- Big Market Orders

Exchanges accept two main types of orders: limit orders and market orders. With limit orders, the customer specifies a “not to exceed” price for purchases and an “at least” price for sales. Market orders on the other hand, instruct the exchange to transact the customer’s entire order as soon as possible at the “best available” price. The disadvantage of a limit order is that it may not execute at all, or may only partially buy or sell the number of shares in the order. Market orders on the other hand are guaranteed to fill, but shares in the order may trade at different prices (almost always worse for the customer) than the price the security was trading at when the market order was entered.

Market makers publish their various bid and ask prices for securities on exchanges, along with the maximum number of shares that are offered at those prices. These published commitments are called the book. For an example book, see “How to Trade ETPs Without Getting Fleeced”.

In the last twenty years, coincident with the rise of High-Frequency Trading (HFT), the typical number of shares posted on the book has decreased. Liquidity providers, like market makers and HFT firms, have decreased their book share size commitments, to enable them to profit from fast market moves. With fewer shares offered on the book, a large market order can quickly exhaust the offers near the current prices. The exchange will then continue executing book offers until all the shares in the market order have been traded—at increasingly worse prices. The IV price of the security is not a factor at this point; the market is just reacting to a short-term imbalance between supply and demand.

Large market sell orders can drop prices enough to cause cascades of additional sell orders triggered by stop-loss orders other traders have put in place—further driving down prices. These mini flash-crashes can drive an ETP’s trading price well below its IV price. Authorized participants are unlikely to act fast enough to prevent these dips, but probably intervene fairly quickly to pull prices back up towards the IV level.

Large market buy orders can have similar effects, causing a security to trade above its IV value, but this scenario lacks the “pile on” dynamic, because if anything, traders will have standing orders to sell a security if it exceeds a specified price, which would tend to dampen price increases.

- Chaotic Market Conditions

The market for a security can be disrupted by any number of things, including technical problems, supply/demand imbalances, or exchange circuit breakers that halt trading for defined intervals when a security’s percentage price drop exceeds a preset threshold. If a disrupted security is included in an ETP’s index, it creates several problems for the ETP’s Authorized Participants.

If trading is halted on a security there’s no current price. Only the last trade price is available, so the IV price of the ETP cannot be precisely calculated. In addition, if the AP would like to do an arbitrage trade, they can’t buy or sell the security as they normally would as part of that trade. If the halted security is a small percentage of the overall ETP’s value, or if an alternate is available (e.g., an equivalent future), the AP might go ahead with the arbitrage trade without it, but the AP might very well wait until trading resumes, allowing the trading price of the ETP to further stray away from its IV price.

If the security is trading, but at a price that’s significantly different from recent trades the APs also have to consider the risk of the exchange’s management busting that trade later in the day. Exchanges reserve the right to bust trades to deal with things like software malfunctions or market makers failing to maintain an orderly market, but with chaotic markets, it’s often difficult to predict what exchanges will later see as an unreasonable price. If a portion of an arbitrage trade is busted it could result in a large economic loss for the AP. Faced with this uncertainty, the natural tendency of an AP is to stay on the sidelines, even if the security is trading far away from its IV price when market conditions are chaotic.

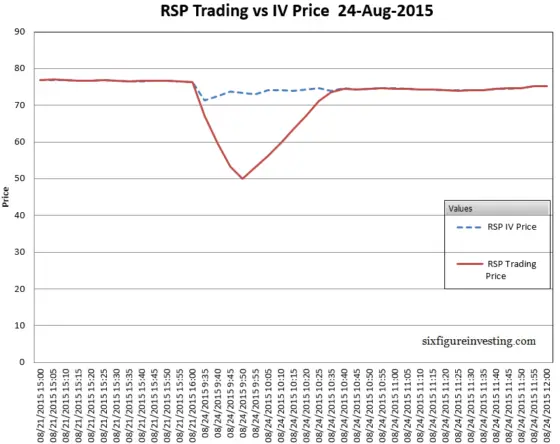

At market open on August 24th, 2015 the market was down sharply, and multiple securities in the S&P 500 weren’t trading due to opening order imbalances and circuit breakers being triggered. Most, if not all of the APs associated with some ETFs including Invesco’s RSP equal-weighted S&P 500 were on the sidelines, not doing arbitrage. RSP’s trading price dropped much more than its IV price, at one point trading at more than a 40% discount. After about an hour, things had stabilized and the ETF was trading back in line with the IV price, but investors with stop loss orders triggered by the unfounded drop in the trading price were sold out of their positions at prices well below the IV price.

Medium Term Dislocations Between Trading Price and IV Price, Hours to Days

Dislocations between the trading price of an ETP and its IV price that persist for multiple hours are usually due to one of the following:

- The activity is outside of regular market hours, during per- or post-market trading periods

- Some or all of the securities referenced by the ETP are traded in markets where their trading hours don’t exactly match the USA trading hours.

Generally, Authorized Participants are only active during the regular trading hours of USA exchanges. Outside regular USA trading hours, ETP prices are driven by the forces of supply and demand, not mitigated by the corrective actions of the APs. If an ETP tracks securities that trade in foreign markets, with different trading hours, then APs will typically only do arbitrage operations when the regular trading hours of the securities overlap.

Long Term Dislocations Between Trading Prices and IV Prices, Months to Indefinite

Significant longer-term differences between trading prices and the IV prices are usually due to one of the following:

- Geopolitical disruptions in the markets where securities that the ETP references trade (e.g., Russia-Ukraine war).

- The requirements that the ETP issuer has put in place for the share creation process are expensive. This happened with Credit Suisse’s TVIX and XIV products between 2012 and 2018. In this situation, the APs would lose money if they attempted to keep the ETP trading around the IV price. To compensate for expensive creates, the APs shift the price point they do arbitrage around higher than the IV price (e.g., 8%). This offset will tend to be relatively stable, depending on the costs associated with the creation process.

- The share creation process has been halted by the ETP issuer. This is the most common and most impactful reason for long-term tracking problems by ETPs. The next section goes into this case in detail.

When an ETP issuer shutdowns the share creation process it can be permanent (for example if the issuer has decided to exit the business), or provisional. The causes of provisional halts to share creations include:

- Futures position size limits have been reached (e. g. , Aug 2009 $UNG)

- Limits on the number of ETP shares that can be issued have been reached (e.g., March 2022 VXX, OIL)

- Risk or capital issues internal to the issuing company (e.g., Feb 2012 TVIX)

In all the situations I’m aware of, the issuer halted creations, but not redemptions. Since share redemptions are still available, APs can still do arbitrage if the ETP’s price is trading at a discount to its IV price, but when creates are not available, arbitrage cannot be used to drive the ETP price down to the IV price. For a current list of ETPs on the New York Stock Exchange that have shutdown their share creation process see Exchange Traded Products – Funds Closed to Creation.

This is a very unstable situation. With no arbitrage available to limit the premium above the IV price, there’s no limit on how high the trading price of the ETP can go. So why would people be willing to pay far more than IV price for a share of an ETP? Greed, of course.

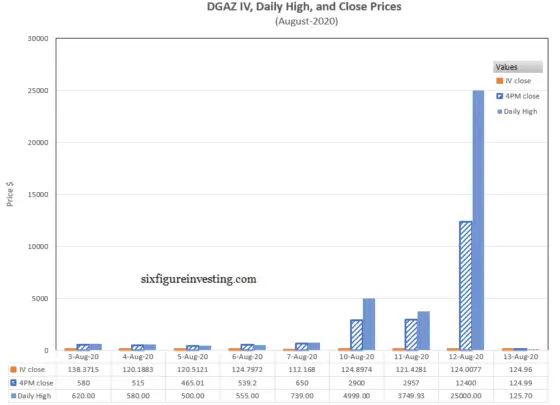

In July 2020 Credit Suisse suspended share creations on nine ETNs, including DGAZ (an inverse 3X Natural Gas ETN) and TVIX, and delisted them on national exchanges. This move signaled the eventual demise of these products, but rather than terminating these funds immediately, which is the typical action by a corporation closing out an ETP, Credit Suisse made a legal, but ugly decision. They delisted the ETNs from the national exchanges like the New York Stock Exchange but did not terminate them.

Credit Suisse did not terminate these ETPs because the termination process requires the issuer to redeem the shareholder’s shares in exchange for cash using the final IV value for the fund. At the time of the delisting, this was a liability of several billion dollars. Instead of terminating the funds, Credit Suisse bet that the IV price of these ETNs would drop over time (a good bet given the characteristics of most of these funds). This will likely reduce Credit Suisse’s liability to near zero by the time (between 2030-2032) that these notes are legally required to terminate. Credit Suisse reserved its right to terminate these funds at any time.

This move by Credit Suisse left these ETNs partially operational, with redemptions still available. After the delisting, trading on these securities moved to the over-the-counter (OTC) markets. In OTC markets the broker-dealers interact directly with traders, buying or selling limited amounts of securities at published prices.

It took less than a month after delisting for trading on DGAZ to become unhinged. With the premium of trading prices unconstrained by APs, DGAZ’s trading price in August 2020 jumped over 40X, from an already inflated $580 per share to a peak of $25,000, while its IV price declined from $138 to $125.

Some of DGAZ’s upward jump was likely driven by margin calls, where traders short DGAZ had their positions closed out by brokers covering their positions by buying shares at ever higher prices. Being short an ETP when the share creation process is not working is an exceptionally risky situation. Credit Suisse brought this circus to a very abrupt halt by terminating DGAZ in August 2020. Termination immediately reset the inflated trading price of DGAZ back to its IV value.

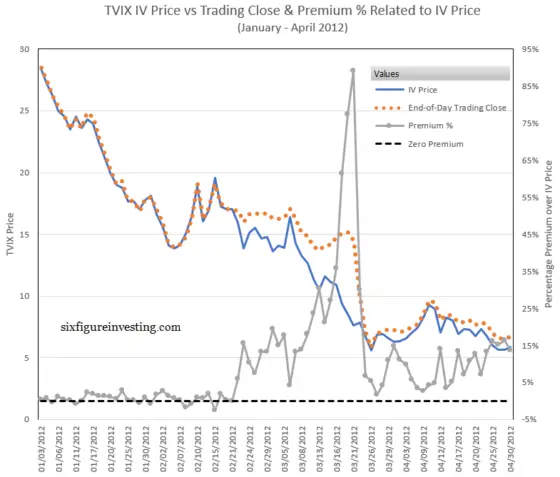

If the ETP issuer manages to fix their share creation problem, then APs can quickly drive the price back towards the IV price (March 2012 TVIX). The chart below shows how this scenario played out for Credit Suisse’s TVIX in 2012.

Credit Suisse announced a halt to TVIX’s share creations on 22-Feb-2012. TVIX’s trading price premium over the IV price immediately started climbing, reaching 90% before collapsing when share creations resumed on the 22nd of March.

Conclusion

Exchange Trading Products have been wildly successful, gathering trillions of dollars in assets. They are tax efficient, offer a wide variety of investment choices with stock-like attributes, and their fees are often very low. Putting processes in place to enable institutional price arbitrage around the ETP’s IV reference price was an essential part of that success. Arbitrage processes associated with ETPs typically work quietly and effectively behind the scenes, but occasionally they glitch and sometimes they break.

In general, it’s ok to ignore the AP behind the curtain, but It’s never a bad idea to check to make sure the trading price and the IV price of an ETP are close together before making a trade, and if you hold a position in an ETP that has halted share creations it’s time for some serious risk analysis.

Click here to leave a comment