In the aftermath of the 2010 Flash Crash, the SEC investigated ways to prevent the widespread disruption of prices that led to trades at absurd levels. One of the outcomes was the creation of single-stock circuit breakers across the entire market (SEC document). These breakers are designed to halt trading at specific points to allow markets to stabilize before restarting. Bigger drops triggered longer waits between restarts.

On Monday, August 24th, 2015 we saw a test of these circuit breakers for Exchange Traded Funds (ETFs). They failed miserably.

Things weren’t as bad as the 2010 Flash Crash, but that’s faint praise indeed, and it wasn’t just small, low liquidity funds that suffered.

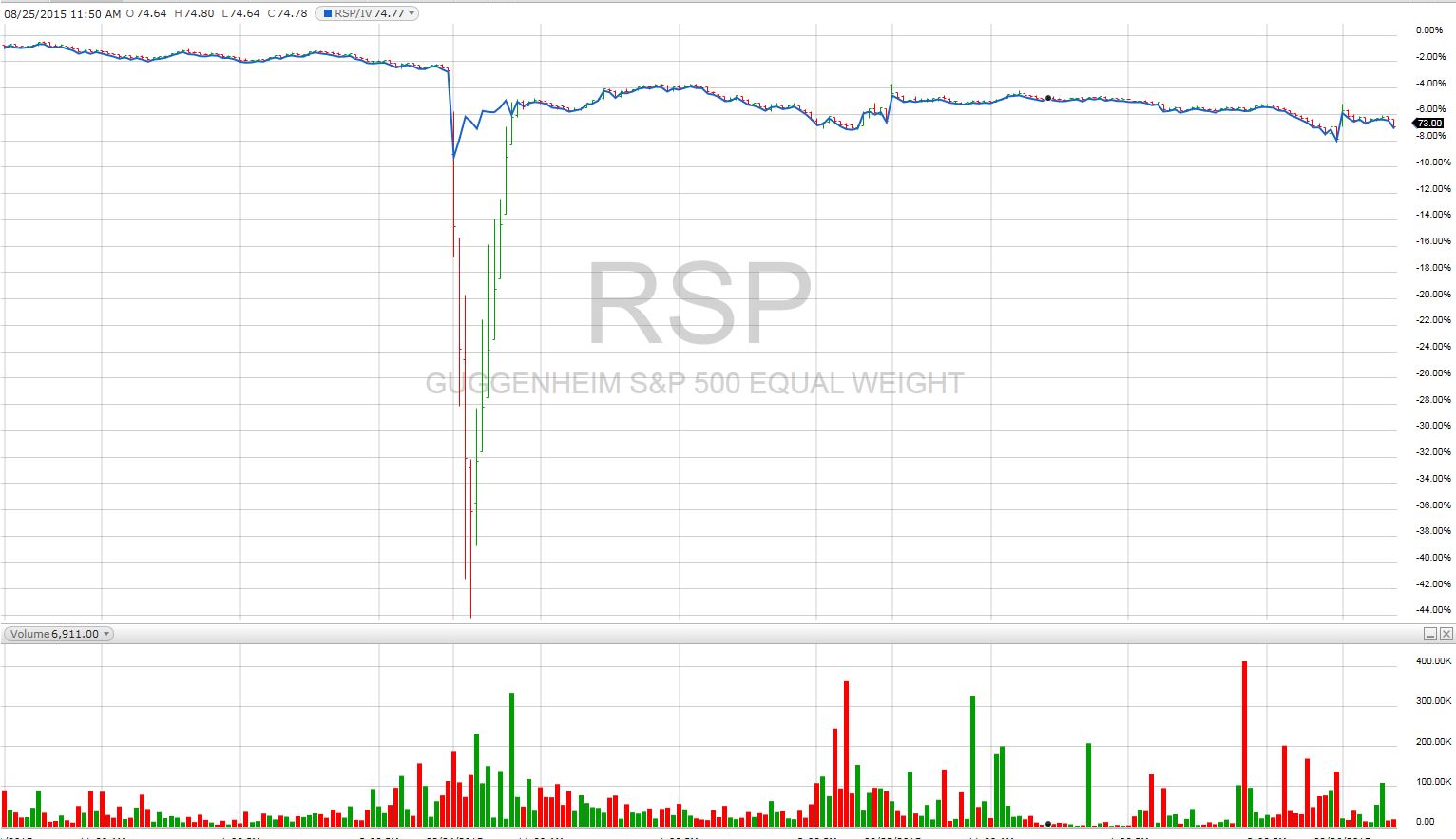

Guggenheim’s S&P 500 Equal Weight ETF (RSP) has $9.5 billion in assets, yet look at what happened on the 24th.

A 38% drawdown from its opening value.

David Nadig from ETF.com does an excellent detailed analysis of what happened with RSP in Understanding ETF Flash Crashes, including the action of the SEC-mandated circuit breakers that “moderated” the crash.

The bottom line is that the essential 2nd tier of liquidity providers for this ETF, the market makers / authorized participates were on the sidelines during this flash crash.

The first tier of liquidity is provided by the people/ institutions that want to buy or sell the ETF itself. With an ETF there is a second level of liquidity providers that steps in if the trading price of the fund starts deviating significantly from the prices of the securities that underlie the fund. These providers earn risk-free profits by buying the underlying securities when relatively underpriced while simultaneously shorting the ETF or selling the underlying short when underpriced by the ETF and buying the ETF shares.

This action by the 2nd tier participants typically keeps ETFs trading close to their intraday indicative value (IV) — which is an index provided by all ETFs that computes the value of the underlying assets of the fund every 15 seconds. The chart below shows the IV values of RSP compared to its traded values.

The value of RSP’s underlying assets, its IV price, only went down 3.1% during the crash.

So the 2nd level liquidity providers were missing in action. In fairness the IV values were probably not an accurate estimate of the prices of the underlying securities at that point—their bid / ask quotes were much wider apart than normal. But even taking that into account the drop in value of RSP’s assets was nowhere near 38%.

Given the chaotic nature of the market, I don’t blame the market makers from stepping back until things settled down a bit. This report from iShares adds a considerable amount of detail on what happened.

Clearly, the SEC did not foresee this situation. The circuit breakers algorithms naively assumed that the listed quotes were representative of the value of the fund’s asset during chaotic times.

Obviously, the SEC’s circuit breakers are a work in progress and aren’t working acceptably. I think the next step should be to incorporate the IV value of the fund into the circuit breaker calculations. Trading halts should be continued when the tracking error between the IV value and the quoted price exceeds some multiple of the normal tracking error, maybe 5X. This would protect investors from being sold out at obviously bogus values.

Excellent approach to the topic, Vance.

Something simillar happened to NYSEARCA:SPYG. From 95 to near 70 in some minutes. Beware of recommending setting stops before leaving on holidays, ha, ha.

But the one million-dolar question is, IMHO, why the other S&P 500-related ETFs did not fail at all.

Anyway, let’s pay atenttion to the next flash crash if this is far from being solved, one “El Dorado” out of a thousand days.

Congratulations for your fantastic site, BTW, I learned the hell reading your posts!

Hey Vance, what do you make of today’s action when VIX was down 14% and SVXY and XIV were down too.

Sometimes the SPX option market which drives the VIX value has a different opinion on things than the VIX Futures market which drives the volatility ETP products like VXX. It’s not clear if one market is more savvy than the other, but I favor the VIX futures market slightly.